- mail us help@24marketresearch.com

- Int'l 1(332) 2424 294 (Int'l)

TOP CATEGORY: Chemicals & Materials | Life Sciences | Banking & Finance | ICT Media

The Electric Vehicle (EV) Construction Vehicles Market encompasses the development, production, and deployment of electric-powered vehicles specifically designed for construction-related activities. These vehicles, including electric forklifts, tractors, trailers, and others, aim to reduce reliance on fossil fuels while promoting sustainability. With a focus on improving energy efficiency, lowering operational costs, and reducing greenhouse gas emissions, EV construction vehicles represent a pivotal shift in the construction industry toward greener technologies.

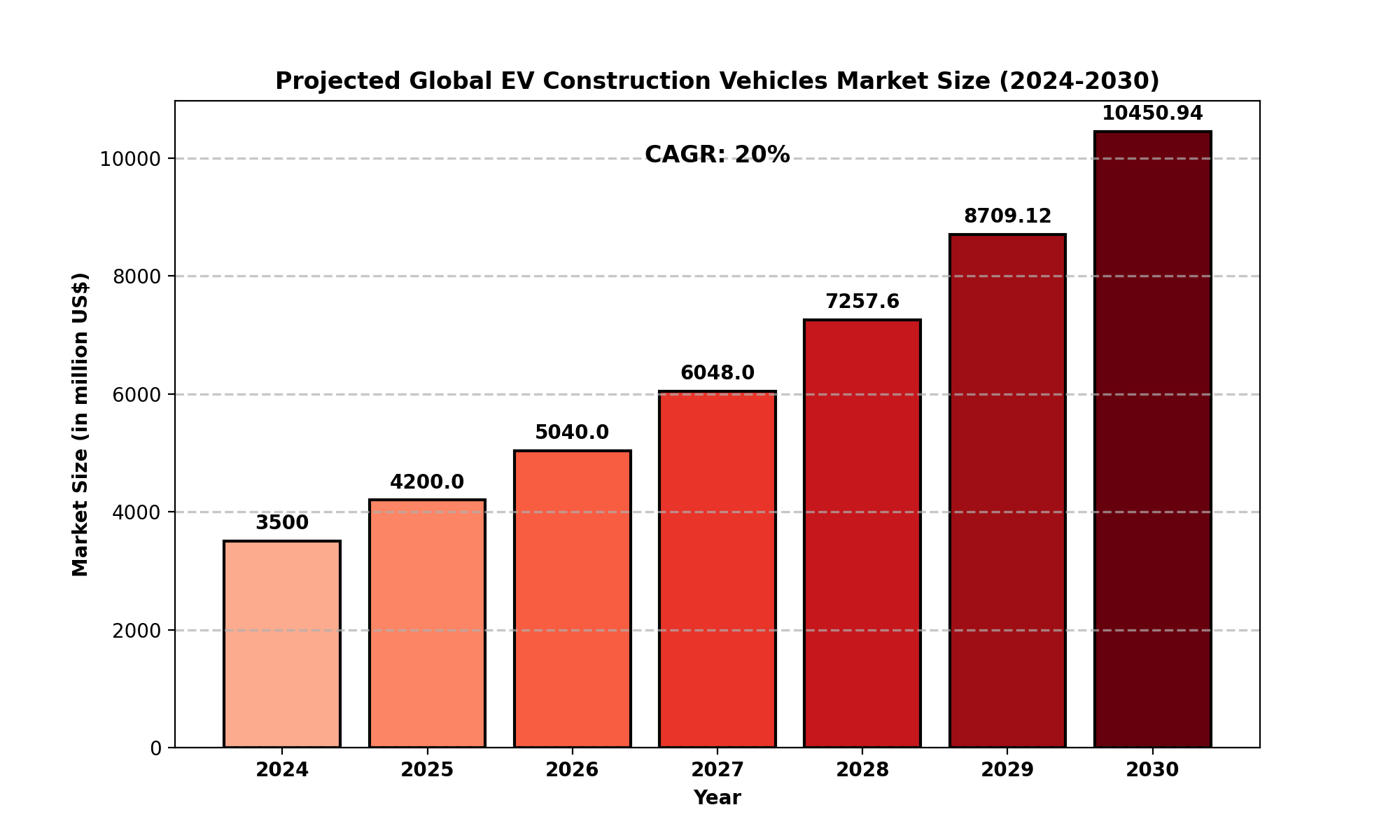

The global EV Construction Vehicles market was valued at US$ 3.5 billion 2024. Projections indicate robust growth, with the market expected to reach US$ 10.4 billion by 2030, exhibiting a Compound Annual Growth Rate (CAGR) of 20% during the forecast period (2024-2030).

This rapid growth is driven by increasing adoption of clean energy initiatives, rising fuel costs, and stringent regulations aimed at reducing environmental pollution. Historical data reflects a steady upward trend in demand for electric-powered alternatives in industrial sectors, with EV construction vehicles gaining a significant market share due to their versatility and environmental benefits.

Environmental Regulations: Stringent government policies on emissions are pushing industries to adopt eco-friendly solutions, boosting demand for EV construction vehicles.

Operational Efficiency: Electric construction vehicles offer lower maintenance costs and higher energy efficiency compared to their diesel counterparts.

Technological Advancements: Innovations in battery technology, such as extended lifespan and faster charging, enhance the appeal of EV construction vehicles.

Cost Savings: Long-term savings on fuel and reduced downtime for maintenance attract significant investments.

High Initial Costs: The upfront cost of EV construction vehicles remains higher than conventional models, deterring some buyers.

Limited Infrastructure: Inadequate charging stations in certain regions pose a challenge to widespread adoption.

Emerging Markets: Developing regions are investing heavily in sustainable construction practices, presenting vast growth opportunities.

Fleet Electrification Initiatives: Increasing adoption of EV fleets by large construction firms fuels market expansion.

Battery Limitations: Limited range and longer charging times can impact operational efficiency.

Market Fragmentation: A highly competitive market with multiple players requires differentiation and strategic positioning.

The North American market, led by the USA, Canada, and Mexico, is characterized by early adoption of EV technologies and substantial government incentives. The USA remains a dominant player due to its advanced infrastructure and large-scale construction projects.

Germany, UK, and France spearhead the European market, driven by stringent environmental policies and significant investment in renewable energy projects. The region is projected to witness steady growth throughout the forecast period.

China, India, and Japan dominate the Asia-Pacific market, supported by rapid urbanization, government support for EV adoption, and an expanding construction industry. China remains a critical market leader due to its robust manufacturing capabilities.

Key markets like Brazil and Argentina exhibit promising growth, driven by increased infrastructure spending and renewable energy initiatives.

The Middle East and Africa regions are gradually adopting EV construction vehicles, primarily through partnerships and government-funded sustainable development projects.

Toyota

Kion

Jungheinrich

Mitsubishi Logisnext

Hyster-Yale

Crown Equipment

Anhui Heli

Hangcha

Doosan Corporation Industrial Vehicle

Komatsu

These players leverage innovation, strategic collaborations, and regional expansions to maintain competitive positioning. For instance, Toyota focuses on hybrid technology integration, while Kion emphasizes battery innovation.

Warehouses: EVs cater to material handling and logistical operations efficiently.

Factories: Deployment in manufacturing units ensures sustainability in operations.

Distribution Centers: Electric vehicles streamline distribution processes with reduced costs.

Others: Miscellaneous applications include construction sites and ports.

Electric Forklifts: Widely used for material handling.

Electric Tractors: Essential for towing operations.

Electric Trailers: Suitable for transporting heavy loads.

Others: Includes niche electric construction vehicles.

Major companies like Toyota, Kion, and Jungheinrich dominate the market. Their strategic focus on innovation, sustainability, and geographic expansion ensures strong market presence and growth.

North America: USA, Canada, Mexico

Europe: Germany, UK, France, Russia, Italy

Asia-Pacific: China, Japan, South Korea, India

South America: Brazil, Argentina

Middle East and Africa: Saudi Arabia, UAE, South Africa

Key Benefits of This Market Research:

Key Reasons to Buy this Report:

Customization of the Report

In case of any queries or customization requirements, please connect with our sales team, who will ensure that your requirements are met.

Chapter Outline

Chapter 1 mainly introduces the statistical scope of the report, market division standards, and market research methods.

Chapter 2 is an executive summary of different market segments (by region, product type, application, etc), including the market size of each market segment, future development potential, and so on. It offers a high-level view of the current state of the EV Construction Vehicles Market and its likely evolution in the short to mid-term, and long term.

Chapter 3 makes a detailed analysis of the market's competitive landscape of the market and provides the market share, capacity, output, price, latest development plan, merger, and acquisition information of the main manufacturers in the market.

Chapter 4 is the analysis of the whole market industrial chain, including the upstream and downstream of the industry, as well as Porter's five forces analysis.

Chapter 5 introduces the latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry.

Chapter 6 provides the analysis of various market segments according to product types, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments.

Chapter 7 provides the analysis of various market segments according to application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.

Chapter 8 provides a quantitative analysis of the market size and development potential of each region and its main countries and introduces the market development, future development prospects, market space, and capacity of each country in the world.

Chapter 9 introduces the basic situation of the main companies in the market in detail, including product sales revenue, sales volume, price, gross profit margin, market share, product introduction, recent development, etc.

Chapter 10 provides a quantitative analysis of the market size and development potential of each region in the next five years.

Chapter 11 provides a quantitative analysis of the market size and development potential of each market segment (product type and application) in the next five years.

Chapter 12 is the main points and conclusions of the report.