- mail us help@24marketresearch.com

- Int'l 1(332) 2424 294 (Int'l)

TOP CATEGORY: Chemicals & Materials | Life Sciences | Banking & Finance | ICT Media

The oil and gas pipeline and transportation automation market encompasses advanced automation solutions tailored for the midstream sector of the oil and gas industry. These solutions include Supervisory Control and Data Acquisition (SCADA), Distributed Control Systems (DCS), Programmable Logic Controllers (PLCs), and other management systems designed to optimize the efficiency, safety, and monitoring of oil and gas transportation.

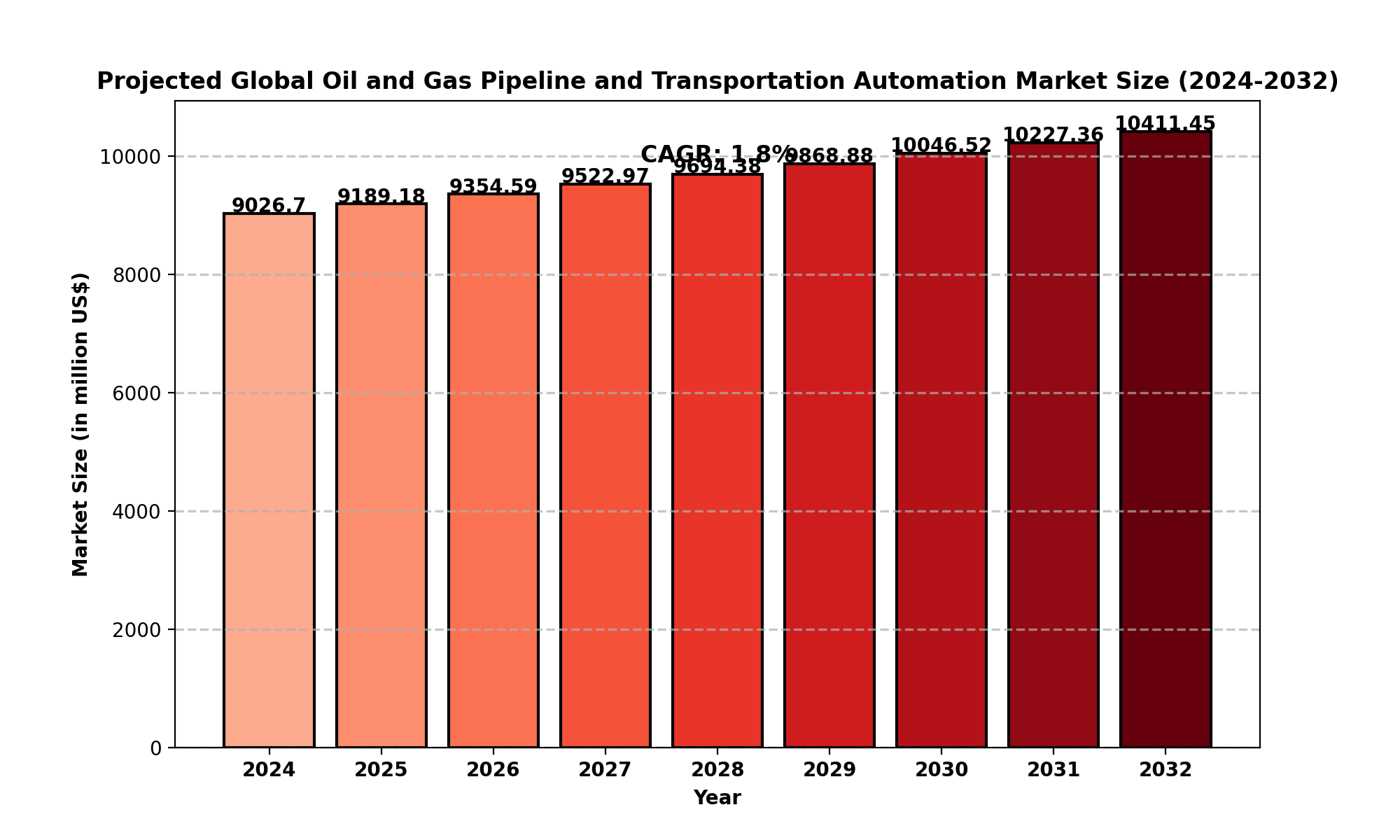

The global oil and gas pipeline and transportation automation market is estimated at USD 9,026.70 million 2024, with projections to reach USD 10,411.45 million by 2032, growing at a compound annual growth rate (CAGR) of 1.80% during the forecast period.

North America’s market size stood at USD 2,425.24 million in 2024 and is expected to grow at a CAGR of 1.54% through 2032.

These figures highlight steady growth driven by increasing demand for energy, modernization of infrastructure, and the need for cost-effective pipeline operations.

Energy Demand Growth: The global increase in energy consumption drives investments in efficient pipeline transportation systems.

Technological Advancements: Innovations in automation technologies enhance real-time monitoring, predictive maintenance, and operational efficiency.

Safety and Compliance: Stringent regulations regarding pipeline safety necessitate advanced automation solutions to minimize risks and ensure compliance.

High Initial Investments: The significant capital required for deploying automation systems can deter smaller players.

Cybersecurity Concerns: Increasing reliance on digital solutions exposes pipelines to potential cyber threats, posing a challenge for operators.

Emerging Markets: Developing regions, particularly in Asia-Pacific, offer growth potential due to increasing energy infrastructure projects.

Integration of IoT: Adoption of Internet of Things (IoT) technologies can revolutionize monitoring and control systems in pipeline transportation.

Operational Integration: Seamless integration of automation systems with legacy infrastructure remains a critical hurdle.

Skilled Workforce Shortage: A lack of skilled professionals proficient in advanced automation technologies affects implementation and maintenance.

Market Share: Dominates the global market with a robust infrastructure and heavy investments in pipeline safety.

Growth Factors: Adoption of advanced SCADA and DCS solutions and regulatory mandates for safe operations.

Market Characteristics: High emphasis on environmental safety and energy efficiency.

Key Regions: Germany, UK, and France lead in adopting automation solutions for pipelines.

Emerging Growth Hub: Rapid industrialization and urbanization in China, India, and Southeast Asia spur market demand.

Infrastructure Projects: Governments' focus on expanding energy infrastructure supports market growth.

Challenges: Economic fluctuations impact consistent investment in automation technologies.

Potential: Brazil and Argentina show promise due to their growing energy sectors.

Market Strengths: Dominated by major oil-producing countries investing in pipeline automation for enhanced efficiency.

Key Drivers: Modernization of aging infrastructure and adoption of advanced technologies.

Key players in the global oil and gas pipeline and transportation automation market include:

ABB: Known for innovative automation solutions, ABB offers cutting-edge SCADA and PLC technologies.

Emerson Electric: Provides advanced automation systems emphasizing safety and efficiency.

Honeywell: Focuses on integrated solutions for real-time monitoring and data analysis.

Rockwell Automation: Specializes in automation products tailored for complex pipeline networks.

Siemens: Renowned for scalable automation solutions and digitalization expertise.

Yokogawa Electric: Offers robust DCS and SCADA systems tailored to oil and gas pipelines.

Oil Industry: Automation solutions enhance crude oil transportation efficiency and safety.

Natural Gas Industry: SCADA systems play a critical role in monitoring and controlling gas pipelines.

Other: Includes refined petroleum products and liquefied natural gas (LNG) transportation.

Supervisory Control and Data Acquisition (SCADA): Essential for real-time data monitoring and operational control.

Distributed Control System (DCS): Provides advanced process control for large-scale pipeline networks.

Programmable Logic Controllers (PLCs): Ensures flexible and reliable pipeline automation.

Other: Includes advanced sensors, remote monitoring tools, and safety systems.

ABB

Emerson Electric

Honeywell

Rockwell Automation

Siemens

Yokogawa Electric

North America: USA, Canada, Mexico

Europe: Germany, UK, France, Russia, Italy, Rest of Europe

Asia-Pacific: China, Japan, South Korea, India, Southeast Asia, Rest of Asia-Pacific

South America: Brazil, Argentina, Columbia, Rest of South America

Middle East and Africa: Saudi Arabia, UAE, Egypt, Nigeria, South Africa, Rest of MEA

Key Benefits of This Market Research:

Key Reasons to Buy this Report: